- To be on the safe side, have an emergency fund with enough cash to cover three to six months’ worth of payments on hand.

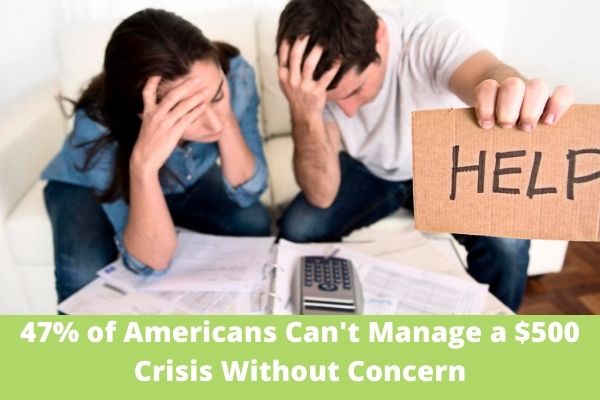

- According to a recent poll, over half of all Americans would find it difficult to come up with $500 on the spot if they were forced to do so.

There is no way to predict when an unexpected bill will arrive in your mailbox or when you will find yourself in a situation where you will be forced to borrow money. Assume you’re a first-time homebuyer.

Various things may go wrong, from a leaking roof to an air conditioner that fails in the summer heat to a broken down car. If you find yourself in this circumstance, you may have no option but to act immediately to resolve the crisis at hand.

You can’t rule out the possibility of job loss, whether it’s entire or partial, as a possibility. Many individuals learned that lesson the hard way due to the epidemic.

That is why it is critical to keep financial reserves available at all times. To be safe, it is recommended that you seek to create an emergency fund with enough money to cover three to six months’ worth of critical costs.

However, according to the Personal Capital Wealth and Wellness Index for 2022, just 53% of Americans are in a position to deal with an unexpected $500 bill without being concerned about their financial security.

That implies that over half of all Americans would be unable to come up with $500 on the spur of the moment. If you fall into this category, you must take action to increase the amount of money in your savings account. Here’s how to do it.

Get on a tough budget.

Follow-through on your budget is an excellent method to keep your expenditures under control and release funds for savings objectives. And it might be your ticket to significantly increasing your savings in a very short period.

If you don’t already have a budget in place, find out the most efficient approach to creating one. That may include pulling out a notepad and jotting down a list of your costs, or it could entail keeping track of your expenditures using a spreadsheet.

It also pays to experiment with the many available budgeting applications. The advantage of taking this method is that many of those applications will connect to your bank account and credit cards, allowing you to classify transactions as they are made, making it simpler for you to keep track of your spending and remain on budget.

Get a second job

It’s possible that a side business can help you save more money more rapidly if you’re severely low in financial reserves and already live frugally (such that even with a budget, your expenditure may not decrease all that much).

In today’s gig economy, there are several options to earn additional income on top of your regular salary, so it pays to shop around or try out a variety of tasks.

For example, you may begin by working retail shifts on weekends only to discover that this does not work well with your schedule. Assuming this is the case, there’s no reason why you shouldn’t experiment with more flexible side employment.

Also read: Special stimulus check payments above $1,261 are available – Do You qualify?

Bank your reward cash

Throughout the year, you may get more funds, whether in the form of a tax return or a gift. However, if you are low on financial reserves, holding your bonus money in the bank may be a better option for you than spending the money.

If you’re working a second job to supplement your income and wish to reduce your working hours temporarily, doing so may relieve some of the stress you’re feeling at the moment.

In the case of an unexpected cost, having a well-stocked emergency fund may help you maintain your financial stability while avoiding a slew of undesirable outcomes, such as unsafe debt.

If you have some catching up on your savings, be sure to put these suggestions into action. It is likely that the sooner you finish your emergency fund, the better you will feel about your overall financial situation.

Make up to 5% back and wipe out interest until 2023

In-house credit card expert recommends this top credit card option because it offers a zero percent intro APR until 2023, which may help you avoid interest payments on new purchases while also allowing you to pay off debt more quickly utilizing easy balance transfer tactics.

Additionally, this selection offers an incredible cashback rate of up to 5 percent with no annual charge. This card is so fantastic that our credit card expert uses it himself on occasion.